Loan Origination involves loan application by the borrower to the sale of the house and everything in between! The entire loan origination process is governed by a loan origination system that is devised by lenders according to their company policies, but more or less follows the same steps From our previous blogs, you might’ve seen how platforms like inflooens are transforming the mortgage industry by making digital loans a reality. For future-ready lending, the loan origination system needs to be truly digital. This means that all steps of the loan origination process need to be connected to a single Mortgage LOS platform that provides reliable and efficient performance. Let’s have a look at how the best mortgage LOS platforms like inflooens make this possible.

The Loan Origination Process

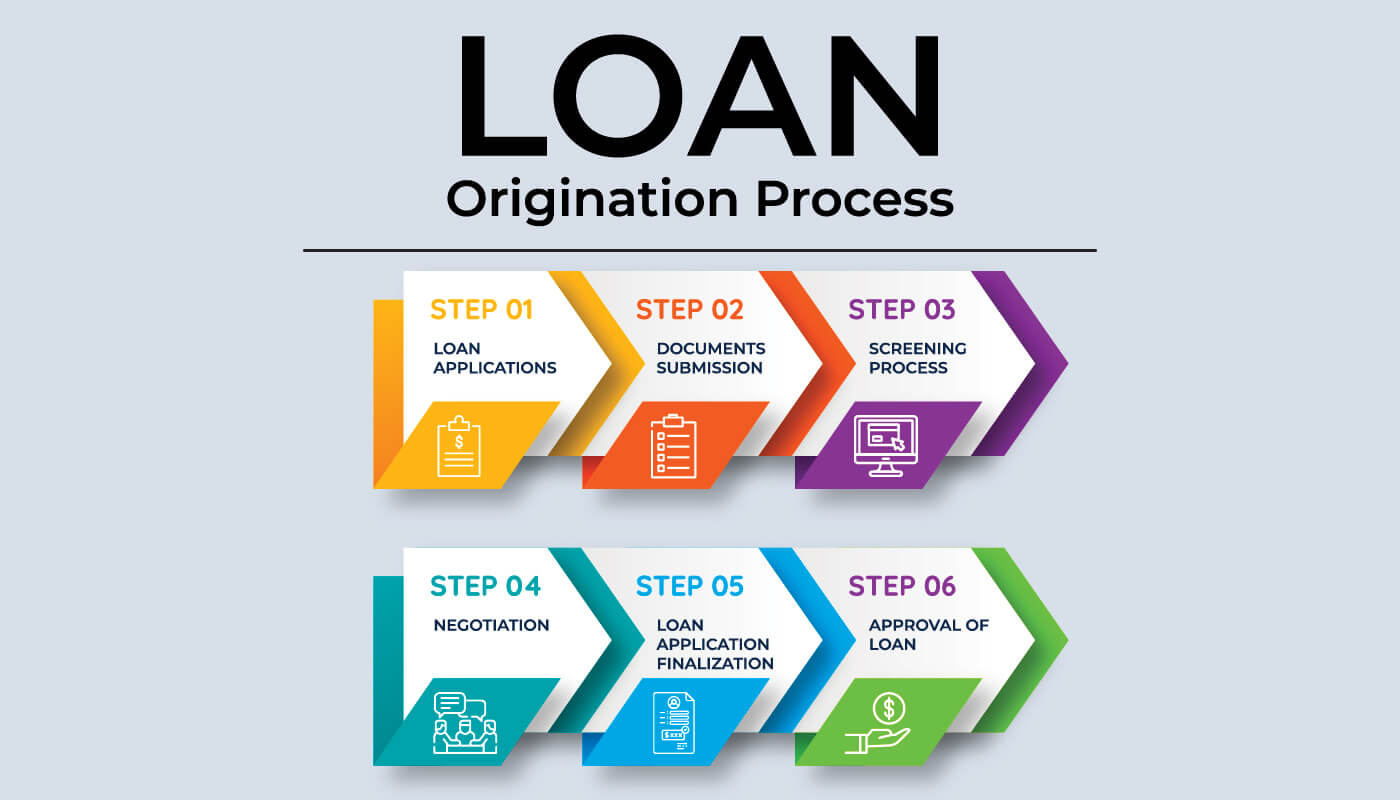

The Loan Origination Process consists of many activities and workflows. We can broadly classify the entire process into 6 key steps as depicted in the image below.

With conventional Loan Origination Systems in the mortgage industry, these processes are inefficient, involve a lot of paperwork, and operate at a snail’s pace. There is huge scope for improvement with digitization and technologies like artificial intelligence, blockchain, and mortgage process automation.

Transforming the Mortgage Lifecycle with Loan Origination Systems

In this section, we will see how each step of the mortgage lifecycle can be transformed. We will look at each step of the Loan Origination Process and discuss how it can benefit from the best mortgage LOS like inflooens.

- 1.Loan ApplicationWith dozens of forms, documents, and paperwork accompanying each application, it is a difficult task to maintain records. Sometimes documents may be misplaced and the borrower needs to submit a fresh set of paperwork, which only delays the loan approval process. Tons of paperwork is also tedious for a borrower as it has to be physically submitted with the lender.

With digital loan origination systems, the entire application process can happen online. Borrowers can submit documents from the comfort of their own homes, without having to visit the lender. For the lender, paperless offices can become a reality as all records are securely stored in the online Mortgage LOS for their reference. This also reduces the time spent searching for documents. - 2. Document SubmissionBorrowers may be asked to submit further documentation like their credit history, bank statements, asset records, job details, etc. This is required to assess the eligibility of the applicant for a home loan.

The best mortgage LOS can not only initiate the process of document collection and storage it can also automatically detect any missing documents in a loan application. This saves the lender and borrower the hassle of back and forth communication to get the paperwork in order. - 3. Screening ProcessThe Screening Process involves ascertaining borrower eligibility. In a digital loan origination process, automated workflows can be used to determine the eligibility of an applicant. For example, borrowers with a low credit score or bad credit history such as loan defaults will automatically be rejected. An intelligent system can be programmed to flag specific cases that may need the intervention of an underwriter to determine the eligibility of an applicant. This reduces a lot of workload for lenders needed for sorting and assessment of applications. Lenders can spend more time on borrowers that will be promising for their business.

- 4. NegotiationIn this stage, an applicant has been shortlisted for a loan, but the amount and interest rate of the loan is yet to be finalized. Many rounds of negotiations may take place between the applicant and the lender to determine the best deal for both parties.

A digital Loan Origination System can help by recommending the best pricing for a particular applicant. For example, if an applicant with a low credit score has applied for a loan amount outside his eligibility criteria, the best mortgage LOS will suggest the lender to negotiate a lower amount with the borrower. This way potential business may not be completely lost. - 5. Loan Application FinalizationAfter negotiation, the amount and rate of interest are confirmed. Usually, the borrower is sent an offer letter by the lender finalizing the terms of the mortgage. This process can be digitized with automated emails that are personalized for the borrower.

The task of painstakingly typing an email to individual borrowers can be taken over by the loan origination system, making the task of lenders easier. An automated system also helps in reducing errors in such critical emails. Furthermore, it can be nerve-wracking for the borrower to wait for emails. On the other hand, it might not always be possible for loan officers to contact the borrowers and inform them about the status of their application. The best mortgage LOS platforms provide automatic status updates to customers and loan officers to maintain a transparent and hassle-free process. - 6. Approval of LoanOnce the loan is approved, the process for crediting the loan to the borrower or seller of the property begins. This stage again involves paperwork to formalize the mortgage. Borrowers and lenders need to sign documents to finalize the mortgage. Loan origination systems can play an important role in automatically creating agreement documents based on standard templates. Additionally, record keeping of all these documents and extremely sensitive documents such as deeds of the property can be done by Mortgage LOS. Some lenders are going a step further and making fully digital loans possible. This enables the borrower to digitally sign loan agreements and the entire process takes place on a secure LOS platform.