Most of the founders are coders, designers, marketers, and folks from different professions. One critical thing that most founders aren’t the best at are the basic legalities when it comes to starting and registering a business.

Let me tell you how important it is to be on the right side of the law. The last thing that you want is getting penalised over a legal mistake that you were not even aware of!

I know that your initial focus is to give shape to your business idea and build a team that believes in your vision. Pitching to prospects, closing deals, and meeting with investors along with developing the product takes up all your time.

However, when you embark on your journey as an entrepreneur, the first thing you should do is register your company.

As a rule of thumb, you should never use your private bank account to make a business transaction. You never know when this could bite you in the future.

Additionally, if you’re looking to raise funding, investors would never invest in a startup that is not registered. Or in case of the incorrect company structure, they would ask you to first get this sorted.

In this article, in order to prevent you from making registration blunders, I’m sharing all that you need to know when registering your company in India.

How to choose your company name

Just as building a business is not easy, coming up with a name for your venture is equally difficult. It takes time to find a name relevant for your business and rushing into a name for the sake of getting the website live does more harm than good.

Think of Google or Nike.

People remember and associate brands by their names. The process of naming a business is equivalent to laying the base of a building.

The name should be strong and well-aligned otherwise it would be remembered for all wrong reasons.

To avoid messing up with the name of your company, take into consideration the following points before registering the company name:

To avoid messing up with the name of your company, take into consideration the following points before registering the company name:

- Choose a name that is easy to remember, pronounce and is short enough to communicate your brand to the customers. Stay away from complex words so that it’s easy to convey the name even on phone.

- The name should reflect the mission of your business. Let the name showcase what the company is all about and the products your company sells. The last thing you’d want is people to think of cars when your business is into selling food.

- Choosing a brand name that sounds similar to an existing player is a bad idea. Hire a lawyer to review the name before you register the company. In many cases, brands have had to change their names because of extreme similarities. You don’t want to face this when you’ve spent millions of dollars over marketing the brand.

- Check if the domain name is available. In this age where a brand has to be present online, if the domain name is already taken by someone else, it doesn’t make sense to choose that company name.

Also, there are numerous extensions to the domain name available. If you’re doing business in India, a .com or a .in is preferred. If you’re going to go global, you may have to add an extension based on the country you’re targeting.

Guidelines for naming a company

Some of the directions of naming a company based on the Companies Act 2013, and Companies Incorporation Rules 2014 are:

- “The Company who deals with financial activities need to have a name related to financial aspects.

- Few names need the approval of Central Government that holds Union, Prime Minister, Statutory, Scheme, National, Small Scale and Federal.

- All of the Company established as a Nidhi can include the words Nidhi Limited at the end of the company name.

- The name should be in resonance with the principal object of the company.

- Name which includes the word Insurance, Venture Capital, Bank and Mutual Fund need to get regulatory compliance from the regulatory bodies like SEBI, IRDA and RBI.

- You can change the name only after three years.”

Limitations on naming a company

- “Generic names which have the places name or other general names are not allowed.For instance, names like solar power, corporate technology, Karnataka business is not allowed.

- A proposed name should not violate the emblems, trademarks or include offensive words.

- A name cannot imply a foreign embassy or foreign government.

- The name cannot be used if it’s similar to a limited liability partnership name.

- The proposed name is identical to the company name dissolved as the liquidation results.

- The Government Company can only utilise the term State in its name. Few instances are Karnataka State Tourism Development Limited, Karnataka State Construction Corporation Limited, etc.”

Once you decide the name of the company, the next step is to incorporate the company. The Ministry of Corporate Affairs (MCA), under the Companies Act 2013 has made the new company registration process very simple and efficient. You can get your company registered within seven days. The process is so seamless that you can get the registration done without even going to the government offices!

This is was impossible a few decades ago, but India has gone 90 percent digital and therefore online company registration is made easier. Every document can be filed electronically, and there is no need for people to visit the place of business registration in India.

Different business structures

As a founder, you should be clear about the name and type of your startup. To register to incorporate your entity under a specific business type, you should be aware of the technicalities of each type.

You will have to choose from – sole proprietorship, private limited, public limited, partnership and limited liability partnership.

Before deciding the business type, have a clarity on the kind of business you are into, your goals and objectives since each of these types come with their own legal implications.

According to Section 3 of companies, a company is a legal entity registered and formed under the 1956 Companies Act. Types of business structures in India

Types of business structures in India

There are five main types of companies you can register in India:

- Sole proprietorship

- One-person company

- Partnership company

- Limited liability company

- Private limited company

Sole proprietorship

The sole proprietorship is the easiest form of company registration in India. One person manages sole ownership, i.e., a sole proprietor. If you are looking to have full control of your business, this option serves ideal.

Key advantages of the sole proprietorship

- No government registration required

- No compliances to be fulfilled

- No government regulatory paperwork

- All profits earned are yours

- You do not require double taxation

- Pay income tax returns only on your income

How to register a sole proprietorship company?

Before you register, you need to have the following documents:

- Aadhaar card

- PAN card

- Bank account Registered office proof (rental agreement or utility bills will do)

Once you have these, you can approach any chartered accountant for a registration certificate and you are good to go.

One-person company

A new type of business structure called One Person Company (OPC) was introduced by the Indian government in 2013.

Until 2013, a single person could not incorporate a company, you needed to have a minimum of two directors to do that.

But why would you need to incorporate a company if you are an individual instead of just going for sole proprietorship?

An incorporated company helps entrepreneurs limit their liabilities and also avail certain tax benefits. But with OPC, an individual could incorporate a company and be the sole director while retaining 100 percent of the company.

Other benefits of a OPC

- Lesser compliance compared to a private limited

- Limited liability for directors (meaning the owner’s personal assets wont be at risk in the event of an unfortunate event)

- Legal Recognition

- Makes it easier to get loans from banks

- Complete control of the company

- Easy to manage

How to register a one-person company?

- Obtain Digital Signature Certificate (DSC)

- Obtain Director Identification Number (DIN)

- Apply for Name Approval

- Documents required:

- Memorandum of Association (MoA)

- Articles of Association (AoA)

- Proof of registered office

- Affidavit and consent of director

- A declaration that all compliances have been made

- File all forms with Ministry of Corporate Affairs (MCA)

- Collect your certificate of Incorporation

Approach a CA and they should be able to take care of the entire process for a nominal fee.

Partnership firm

If you decide to have partners in your business, the easiest way to go ahead with is to create a partnership firm. All you need is a partnership deed which is an agreement between the partners. This agreement will contain all the duties and obligations between the partners and how profit will be shared.

Details to be mentioned in the partnership deed

- Name and address of all the partners

- Name and address of the partnership firm

- Starting date of the firm

- Capital each partner has invested

- Profit share ratio among partners

- Salaries/commissions to be paid out to partners

- Rights of each partner

- Duties and obligations of each partner

- Other clauses which are mutually agreed upon

You can register the partnership firm Indian Partnership Act, 1932 but it is not mandatory and is at the discretion of the partners.

Benefits of partnership companies

- Easy and convenient to form

- Risk is shared between partners

- No need to submit annual returns to the MCA

- Statuary Audit is not mandatory

- Easy to wind up

- Flexibility

Limited liability company

Limited Liability Company(LLC) takes advantage of other business structures corporation, partnerships, and sole proprietorship. Limited Liability Company is entitled as flexible business structures, and LLC separates personal and business liabilities. Every owner will have their tax liabilities shared.

LLCs are not liable for business debts like other business structures, and these have limited life.

Key advantages of LLC

- The paperwork in LLC is much lesser as compared to other registrations. This makes LLC more flexible and easier to form.

- LLCs keep their members safe from the liabilities like personal debts and legal hearings.

- It also provides tax flexibility where the income, expenditures, and profits become the part of owner’s tax returns.

- In LLCs, one does not have to necessarily follow a business structure to run one’s organisation.

- Profit sharing is also flexible in LLCs.

How to set up an LLC?

- Apply for DPIN (Designated Partner Identification Number) by filling the form online.

- Acquire your Digital Signature Certificate and register it on MCA portal.

- Get the approval for your LLC name from the Ministry of Corporate Affairs.

- After approval, fill the incorporation form to register the LLC and obtain the LLC agreement.

Private limited company

A Private Limited Company aka LTD is a type of company that has a minimum of two and a maximum of 200 members. As the name suggests, it cannot raise the funds from the public, which means the company cannot publicly issue the shares. There is no paid-up capital required now to set up an LTD.

Some benefits of having a private limited company

- The liability of the company’s owner with respect to the company’s debt is only limited to his/her shares.

- The shares of the company are easily transferrable to the other person.

- The company can issue debentures and can receive funds from public platforms, thus making it easier to raise the money.

- There are more tax benefits in LTDs and the percentage of applied tax is also lesser as compared to other types of company registrations.

How to register a private limited company

- Obtain Directors Identification Number(DIN), which is a unique code that requires you to have a PAN card, Aadhaar card, bank statement, phone and electricity bill

- After that, a name registration application needs to be filed.

- Now, you need to draft MOA and AOA. MOA states the objects of the company while AOA specifies the rules and regulations of the company.

- Now file the application through SPICE-E form on MCA’s website and obtain PAN and TAN applications.

If all your papers are in order, you are done with your application.

Importance of choosing the right business structures

It’s significant to select the business structure carefully as it impacts your income tax returns. Each business structure has its own compliances, and therefore you need to keep this in mind on how to set up a company in India. The company needs to file annual returns and income tax return with the company registrar.

The company’s account books are audited mandatorily every year. The legal complications need spending money on tax filing experts, accountants, and auditors. Choose the right business structure when thinking of registering your company in India.

A businessperson should have a clear idea of the type of legal compliance she/he is willing to take care of or deal with. Some of the business structures are investor friendly while others are complicated. The investor will prefer to go with a legal and recognised business structure.

Here are some crucial questions you should ask yourself before deciding on how to start your company in India. They’re important in deciding the next plan of action.

1. Should your initial investment influence your business structure choice?

Yes! If you need to spend less, then you should go with either partnership or sole proprietorship.

You can prefer to choose a Private Limited Company or LLP in case you can recover the compliance and setup costs.

The cost of registration of a sole proprietor company is nearly Rs 2,500 while that of a partnership firm is nearly Rs 5,000. If you incorporate a private (LLP or LLC) company with a minimum authorised capital of Rs 1,00,000, the registration will cost you Rs 7,000.

2. What are the income tax rates for each business?

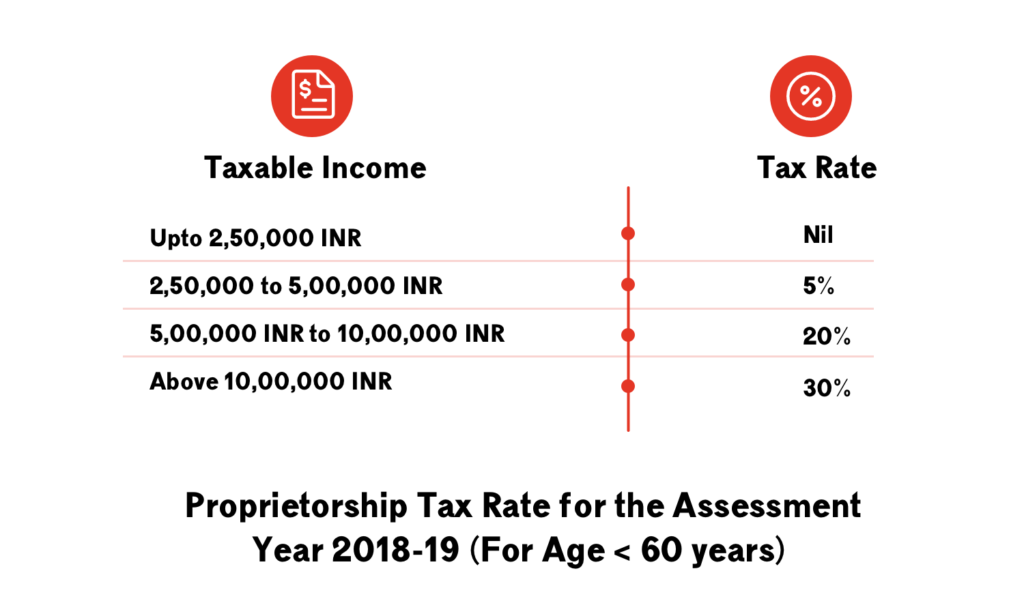

For a proprietor, the income tax returns are similar to the individual income tax return filings.

For an LLP, the income tax returns are filed under the form ITR-5. For the turnover of more than 40 lakhs, you need to get a tax audit.

3. How many partners or owners the business holds?

In the case of an individual managing the entire company then it’s an excellent option to choose a person company. If there is more than one owner, then you can choose a Private Limited Company or Limited Liability Partnership.

4. Are you willing to bear the entire business liability?

HUF, partnership, and Sole Proprietor business structures will have unlimited liability. The money will be recovered from the partners or members in the profit sharing ratio in the case of default loans. The personal asset risk is high in this case. LLPs and companies have limited liability. The member liability is restricted to the contribution amount made by the share value of each member.

5. What are the plans for getting the amount from investors?

Investors stay away from unregistered business structures. Entities like Private Limited Company and LLP are trusted by angel investors and venture capitalists. You should seek the help of a lawyer before choosing the best business structure for you.

6. How to choose the best suited structure?

The three critical factors to look into while choosing to incorporate a company in India are: Taxation: The business owners who desire to report losses and profit of their business on their personal tax returns and who are taxed on the net earnings from the company need to select “pass-through entity”. This includes partnerships, sole proprietorships, and LLC in India. The owner who needs to utilise a corporate structure to take advantage of corporate tax rates should go with C Corporation or S corporation business structure.

Risk: A business is always risky and business owners should consider opting for a business structure capable of securing their personal and valuable assets from the business responsibilities. A corporation or LLC can insulate the personal assets of the owner from the business litigation and creditors.

Complexity: LLCs and corporations need detailed record keeping and adherence to an extensive list of needs to control Limited Liability protection. The additional factors are:

Control: The level of control the business owner has towards the business directly impacts the company registration structure. For example, if you are the business owner who adheres to manage the company as an individual, then you should be ready to stay as a sole trader. Complexity and cost of legal structure and formation: There are various legal structures, and each has an ideal set of complications, procedures, and cost. For instance, a sole trader required few reporting needs that he/she can do by themselves. A more complicated structure like a trust holds requirements of strict reporting and should be set up by an accountant or solicitor.

Tax implications: The business legal structure holds essential effects on the tax amount you pay. A sole trader can enjoy the tax benefits by claiming on a personal tax return whereas a trust does not need to pay income tax on profits.

How to register a company

Here are some of the procedures for registration of the company under companies’ act 2013. There are four critical steps to be followed on how to register a company in India.

- Obtaining DSC (Digital Signature Certificate)

- Obtaining DIN (Director Identification Number)

- Filling a New User Registration or eForm

- Incorporating the company

Obtaining a DSC

The first step is to apply for the DSC of the directors also derived as Digital Signature Certificate. DSC is e-signature which enables you to complete the online company registration process in India. It takes two days to obtain DSC after submitting the documents.

The Information Technology Act, 2000 has included provisions for utilising digital signature on every submitted document in the form of electronics to make sure the authenticity and security of the documents are filed electronically.

This is an authentic and secure way to submit a document electronically. Similarly, all filings done by the LLP and companies under the government program of MCA21 are needed to be filed utilizing the digital signatures by the person who is authorized to sign the documents.

Obtaining DIN (Director Identification Number)

The second step is to acquire an identification number. Obtaining a DIN is mandatory according to the amendment act of 2006. Every intending and existing directors need to acquire DIN. To get this, file a DIN e-form. The form can be taken from the official State of Ministry of Corporate Affairs.

Once receiving the generated DIN, they should let know about their organisation about DIN. The director can let them know about their company using DIN 2 form. The company should then intimate the ROC (Registrar of Corporate) regarding all DIN of the directors via DIN-3 form.

In the case of any changes in DIN or if there is anything to be updated like personal details, address, etc., then the director needs to initiate the changes to be done through the eForm DIN- 4 forms.

Filling a new user registration or e-form

This part is about having an MCA portal or registered user account for e-Form filing, for different transactions, for online fee payment as business and registered user. Creating an account is free.

Incorporating the company

How to get a certificate of incorporation in India? Here you go! The final part of the company registration online is incorporating the company name, notice for appointment of managers, secretary, and company directors, and registering the opinion of the situation of office and office address.

Checklist of documents needed

- DSC – Digital Signature Certificate

- Form – 1 for Incorporation of Company in India

- Form-32 for particulars of managers, secretary, and proposed directors

- Director Identification Number of all proposed company directors

- Original copy of the formal letter which is published by ROC about company name availability

- Form- 18 for address or situation of the proposed company.

Formalities to be followed

- Obtain a TAN card

- Documents obeying act of shop and establishment if required

- Registration document of STPI (Software Technologies Parks of India) if required

- Both foreign and Indian directors need to have authorized agencies digital signature certificates

- Obtain a PAN (Permanent Account Number) from the income tax department of India

- Registration documents of IEC (Import Export Code) from foreign trade director general for international trade if required

- RBI approval for investing in FIPB and India support of foreign companies if required.

So what have you decided? What business structure are you going for and why? Let us know in the comments below

Source at: yourstory.com